There has been a sudden rush of foreign direct investment (FDI) in India’s financial services sector. Some of the world’s biggest financial firms are leading the charge:

- September 23, 2025: Sumitomo Mitsui Banking Corporation (SMBC), Japan’s second-largest bank, invested over $1.6 billion for an approximately 25 per cent in Yes Bank.

- October 2: Abu Dhabi’s International Holding Company (IHC) paid $1 billion for a controlling stake in Sammaan Capital (formerly Indiabulls Housing Finance).

- October 10: The US-based Warburg Pincus, among the world’s top 10 private equity (PE) firms, purchased a nearly 10 per cent stake in IDFC First Bank for Rs 4,876 crore ($587 million).

- October 18: Emirates NBD paid $3 billion for a 60 per cent stake in RBL Bank.

- October 24: Blackstone, one of the world’s three largest PE firms, announced it would buy a 10 per cent share in Federal Bank for $0.7 billion.

- December 22: Japan’s largest bank, MUFG Bank (formerly Bank of Tokyo Mitsubishi UFJ) injected $4.4 billion for a 20 per cent stake in Shriram Finance via a primary infusion.

- February 14, 2026: The Reserve Bank of India (RBI) gives final approval for the US private equity giant Bain Capital to acquire joint control of Manappuram Finance and up to 41.66 per cent of the company’s equity and convertible instruments for $484 million.

This inflow of over $11 billion into the sector in the space of a few months indicates (1) that foreign investors are interested in India’s banking sector, and (2) that the Indian authorities are opening up the sector to foreign investors. Note that banks such as Sumitomo and MUFG are unlikely to be interested in remaining passive investors in Indian banks and NBFCs over the medium term; presumably they are working on the assumption that they can acquire a controlling share after some time.

What is behind these developments? Well-known analysts have given different views on the question.

One interpretation is that these inflows are needed in order to compensate for India’s declining rate of household savings. Ajay Shah argues in the Business Standard says that India’s inadequate household savings “will hamper domestic investment unless restrictions are removed so as to give access to plentiful and low cost foreign capital. The $11 billion inflow in 2025 into one narrow group of firms demonstrates that foreign savings are available, when we remove the restrictions at our end.”[1] The author has long been a believer in the ‘free market’ and the lifting of all capital controls.

Shah traces the sudden inflow to regulatory changes, reflected in the January 20, 2025, Reserve Bank of India (RBI) “Master Direction on Foreign Investment in India”. However, as he observes, it is not only a regulatory change, but a policy shift: “Beyond the text of the regulations, there was a perceptible shift in the supervisory approach. The RBI’s approval of majority stakes, such as the Emirates NBD acquisition of RBL Bank, suggests a new pragmatism.”

Backdrop to policy change: fall in net FDI

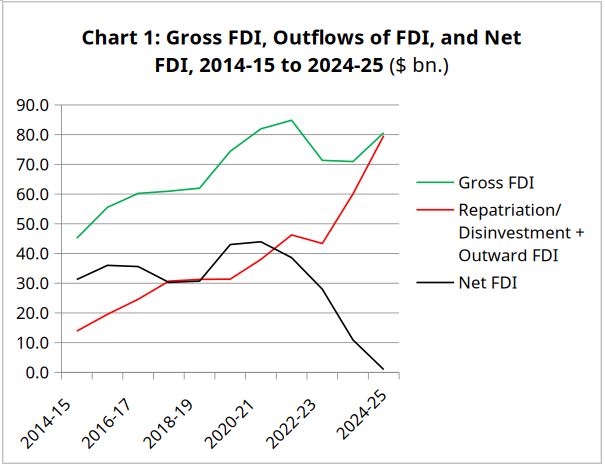

What led to this shift? Shah notes that net FDI into India has been stuck for over a decade, and “By October 2025, net inflows of foreign direct investment (FDI) were not looking good.” He is quite right in this respect. Let us look at this development in more detail, as it is relevant to assessing his propositions, and it may turn out that the solution being offered worsens the problem it is meant to solve.

Net FDI is Foreign Direct Investment into India minus two types of outflows: (1) repatriation/ disinvestment by foreign direct investors who had invested in India earlier; and (2) outward FDI, i.e., direct investment abroad by Indian investors. That is, while some foreign investors are investing money in India, some other foreign investors are taking their capital out of India; and Indian investors are investing abroad. After netting out the inflows and outflows, we get net FDI.

Over the last few years, net FDI has plummeted, falling to less than $1 billion in 2024-25 (see Chart 1). While gross inflows have remained sizeable, repatriation/disinvestment by foreign investors has risen steeply as a share of gross FDI, from 25 per cent in 2019-20 to 64 per cent in 2024-25, that is, nearly two-thirds of the gross inflows![2]

Similarly, outward FDI by Indian investors has risen from 17 per cent of gross FDI in 2019-20 to 35 per cent in 2024-25. Thus the combined outflows on account of repatriation/disinvestment and Indian outward FDI have risen so steeply as to almost wipe out the gross inflows.

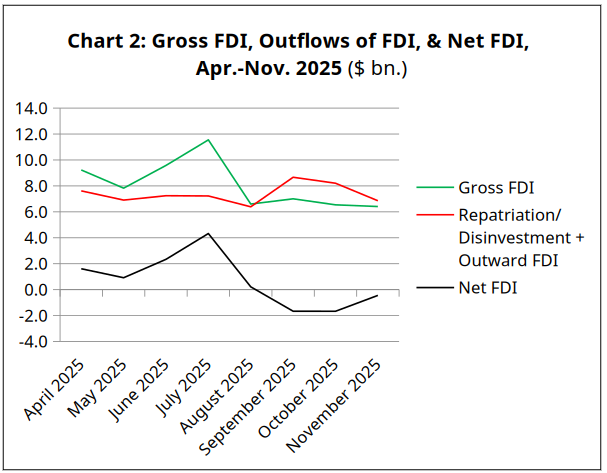

Source for both Charts: RBI database.

This trend has continued during 2025-26 (see Chart 2). In September-November 2025, the combined outflows on account of repatriation/disinvestment and Indian outward FDI were greater than the gross FDI inflows, so that net FDI turned negative in the last 3 months.

Why has net FDI fallen?

Conventionally, FDI is meant to provide not merely capital but a bundle of ‘intangibles’, i.e., such as advanced technology and managerial expertise, that would strengthen India’s manufacturing sector. Thus FDI is said to differ from foreign portfolio investment (FPI), which is a purely financial flow. The efforts of successive governments to attract FDI, such as the ‘Make in India’ programme and more recently the Production-Linked Incentives programme, have done so on the basis of this claim. Further, since FDI is considered a long-term investment, it is meant to be less volatile than FPI.

Significantly, as Biswajit Dhar and K.S. Chalapati Rao point out, FDI has been increasingly concentrated in India’s services sector rather than the manufacturing sector. With growing liberalisation of the financial sector, financial services became “the overwhelming favourites of foreign investors”. Moreover, in India,

serious questions about the utility and reliability of these inflows are beginning to surface. Our detailed research into the essential character of the FDI inflows into India has shown that only about half of the inflows could qualify as real-FDI, that is, they could potentially be the providers of the ‘package of development inputs’, the critical intangibles like technology and managerial skills, besides capital.[3]

Along the same lines, R. Nagaraj finds that private-equity/ venture-capital constitutes a growing share of FDI, rising from about 20 per cent in 2011-12 to nearly 80 per cent in 2021-22. PE/VC “by definition does not invest in greenfield [i.e., altogether new] projects that contribute to potential output. It is used to acquire existing factories, firms and brands, only to quit at the correct stock prices.”[4] Thus in India, to quote Dhar and Rao, “the distinction between direct and portfolio investment can be, at best, fuzzy.”[5] Identified tax havens such as Singapore and Mauritius became the main sources of FDI, rather than countries which might be sources of technology and managerial know-how.[6]

The problem has been compounded by the increasing desperation in official circles to obtain FDI, not for the aim of upgrading India’s manufacturing, but for meeting the current account deficit (CAD) and boosting the foreign exchange reserves. That is, rather than finding ways to increase India’s foreign earnings or curb foreign payments, the Government has been taking on more liabilities to bridge the gap. It cannot afford to look too carefully at the nature of those liabilities.

Hence foreign investors are being increasingly allowed without even minimal review. As Nagaraj points out, the same tax havens which are major sources of FDI are also major destinations of outward FDI, indicating that much of the FDI entering and exiting India may be “hot money”: “Large financial conglomerates move liquid capital across the world to take advantage of variations in tax laws, a practice known as ‘treaty shopping’…. The rising share of outward FDI suggests that India may be used as a conduit for tax arbitrage by international capital.”[7]

As a result of the above policies and trends, then, what is termed ‘FDI’ has proved to be increasingly fickle. Meanwhile, net foreign portfolio inflows (FPI), which are foreign inflows into India’s share markets and debt markets, fell from $41 billion in 2023-24 to $2.7 billion in 2024-25. They then fell further to -$3.9 billion, i.e., net outflows, in April-December 2025.

As capital inflows, both FDI and FPI, have fallen, this has led to downward pressure on the value of the rupee. The rupee fell 5.4 per cent against the US dollar between April 1, 2025 and January 15, 2026, making the rupee among the most-depreciated currencies in this period.

What the above discussion reveals is that FDI itself has become composed of more mobile financial flows, less and less associated with manufacturing and the domestic absorption of capabilities, and more and more concentrated in the financial sector. Out of the $11 billion of FDI inflows into India’s financial sector since September 2025, about half have been made by private equity and other financial investors. Since these inflows are of more mobile capital, we should not be surprised if they flow out.

In effect, when, as a panacea for the outflow of foreign direct investment, which is on account of the increasing share of volatile financial flows in FDI, Ajay Shah recommends opening up further to all types of FDI in the financial sector, he is not advocating it on the ground that this capital will introduce new technology or other know-how, but merely on the ground that it will bring in some more funds. This indeed is also the logic on which the Indian authorities seem to have opened up FDI in banking. In fact it is a recipe for further instability.

Shah contends that finance knows best what to do with resources:

Finance is the brain of the economy. It allocates resources to their most productive uses. These transactions make the Indian financial system healthier. By removing barriers at the border, we have allowed the brain to upgrade its processing power.

Decontrolling the brain (the financial sector) will make the entire economy more efficient. For Shah, this is confirmed by the fact that the stock market rewarded the targeted companies which recently announced FDI.

Unfortunately, history does not bear out his theory. Time after time, financial crises have emerged from the financial sector, particularly when it has been freed of regulatory ‘fetters’. The liberalisation of the American financial system led to an extraordinary financial mania, which ended in the Lehman debacle of 2008. That in turn caused a global crisis. In India, there have been many instances of major mismanagement in non-government banks and NBFCs, such as Yes Bank, IL&FS, DFHL, and recently the treasury fraud in IndusInd Bank. There have also been instances of problems in government banks, but government ownership has reassured depositors, and there has been no contagion fall-out when problems have affected government banks, unlike the private sector.

This is not just a financial sector problem. When the financial sector experiences a crisis, it can strangle credit and derail the entire productive economy.

Only at the margin?

Another leading commentator on banking, T.T. Rammohan, has defended the decision to ‘open up’, arguing that Indian banks, both private and public, are much stronger than in the past: “In today’s setting, foreign banks will have their work cut out in competing with entrenched domestic players. The retail market will be difficult to penetrate without investment in a large network of branches. Without a large network of branches and low-cost current and savings accounts, taking corporate customers from Indian banks too will be a challenge”. Moreover, the banks entering the Indian market, being from Japan, “are far less formidable than a Citibank or a Bank of America,” and some others are purely financial investors. Hence this should be seen as “a welcome infusion of patient capital into banks that need more capital.”[8]

Rammohan himself acknowledges that, in the past, India’s regulators were concerned that, in any international crisis, foreign banks may face a capital crunch in their parent countries. In such a situation they may reduce lending and tighten credit standards in their Indian operations. This would make India more susceptible to shocks from the international financial system. However, he dismisses such concerns today, since foreign banks account for less than 7 per cent of the assets, and “there is little chance of their market share rising significantly in the medium term. Any withdrawal on their part from the credit market will not make a big difference to aggregate credit supply.”

Why India was relatively less affected in 2008

In fact, the reason India was relatively less affected by the 2008 Global Financial Crisis was that its financial sector was relatively less integrated with global finance than was the case with many other countries. Part of the credit goes to Y.V. Reddy, the then governor of the RBI, who recognised the risks in opening up to foreign banks, who “operated across borders, and across markets, through multiple organisational layers within a conglomerate. They had a network of non-banking arms operating in parallel in India…. Cross-border presence gave them an opportunity to move financial assets across the border to take advantage of differences in regulation, taxes, and interest rates.” When, in 2003 and 2004, two successive finance ministers announced they were raising the limit on FDI in banking to 74 per cent under the automatic route, and pressed Reddy to implement this, he found creative ways to frustrate their decision, as he describes in his memoir.[9]

In the period since 2008, however, the Indian economy has gotten more integrated with international finance, as can be seen from the data cited earlier, and any international crisis would get transmitted to India to a greater extent than in the past. Interestingly, Indian banks have been facing a liquidity crisis in recent months, largely due to the outflow of FDI and FPI. This is despite the absence of an international financial crisis. In such a situation, foreign ownership of 7 per cent of banking assets, when combined with a much larger foreign share of the non-banking financial corporations (NBFCs) sector,[10] is already a considerable vulnerability.

Rammohan asserts that there is little chance of the market share of foreign banks rising in the medium term. It is true that foreign banks’ growth is hampered by their incompetence and lack of knowledge of Indian conditions. The recent limited history of FDI in Indian private sector banking does not inspire confidence in foreign investors’ management expertise. In 2018, the Canada-based Fairfax group invested around Rs 1,400 crore ($164.7 million) in CSB Bank (formerly Catholic Syrian Bank) for a 51 per cent stake, and in 2020 DBS merged Lakshmi Vilas Bank (LVB) into its Indian subsidiary DBS India. In the case of CSB Bank, the bank initially recovered, but under a subsequent CEO with private retail banking expertise the bank’s performance has been deteriorating. Meanwhile DBS India seems to have been clueless on how to leverage the erstwhile LVB’s branches, and the amalgamated DBS India has been making significant losses in its retail division after the acquisition. These examples do not convey a favourable picture of the management expertise of foreign banks in India, where conditions for retail banking are very competitive.

However, the growth of the foreign share of the Indian market hinges on the extent to which the Indian authorities allow foreign investors what is called ‘inorganic’ growth, i.e., acquisitions. At present, the scope is limited. Foreign investors, including portfolio investors, can own up to 74 per cent in Indian banks, but regulations at present cap a strategic foreign investor’s stake at 15 per cent. Any holding above 5 per cent requires RBI’s prior approval.

RBI signals change

A partial change may be afoot. In June 2025, RBI Governor Sanjay Malhotra said the RBI was reviewing the ownership structure of banks. “Our economy is growing. We need more banks. Keeping that in mind, if there is a need for change, it will be done.” While he clarified there was no immediate change in the overall policy regarding the cap on foreign investment, exceptions could be made on a “case-by-case” basis.[11]

Without the prospect of greater control, it is unlikely Sumitomo would have invested in Yes Bank: it does not make sense as a pure financial investment. Meanwhile, Canada-based Fairfax Financial Holdings is considered a frontrunner for the Government’s majority stake in IDBI Bank, which has undergone a clean-up and returned to profitability. In this fashion, the “case-by-case” exceptions may increase, and that would increase the market share of foreign-controlled banks.

Unlike Indian private sector banking, where managerial authority and hierarchy resides within the pyramidal organisational structure in India, foreign banks operate on verticals aligned with their global structures, and hence authority for managerial decision-making in India may reside outside India and outside the purview of the RBI. In that case the impact of decision-making abroad on Indian banking would be larger than it is now. For example, in case of a crisis abroad, foreign banks may restrict their lending in India, which would have an impact on liquidity here.

The authorities’ argument for “reviewing the ownership structure” is that a growing economy’s credit needs require additional bank capital. The question is: if private banks are at present unable to cater sufficiently to the credit needs of the economy, why turn to foreign capital? The sovereign Government itself can invest additional capital in the public sector banks instead. The Government’s existing neoliberal policy frame may rule this out, but that is a reason for changing the policy-frame rather than opening Indian banking to foreign capital, which would render India more vulnerable to global developments, in a volatile global situation.

There is little ground to be complacent about Indian policy-makers’ stances regarding the financial sector. Today, the Government has abandoned several settled positions overnight under pressure: it has opened up to agricultural imports from the US, it has given commitments of expanding imports from the US by $500 billion over 5 years, it can no longer decide where it imports oil from, and so on. Moreover, India may experience further capital outflows and uncertainty on the foreign exchange front in the coming period, which would increase the pressure to attract inflows at any cost.

Interestingly, India appears to have dropped its earlier insistence on reciprocal rights for its banks and financial institutions in the parent countries of the foreign investors. Indian banks will continue to be restricted asymmetrically in those markets. This, too, indicates that the decision to open up was not a considered decision taken in the long-term interest, but a decision made under pressure of the collapse of net foreign investment in India.

Notes

- “Gains from decontrol: Removing constraints offers substantial gains,” Business Standard, January 5, 2026, https://www.business-standard.com/opinion/columns/gains-from-decontrol-removing-constraints-offers-substantial-gains-126010400694_1.html . ︎

- Conventionally, one thinks of FDI as representing an inflow of share capital from abroad. However, the official definition of FDI used by India includes two further categories: reinvested earnings, which are generated within India itself; and inter-corporate loans, which are actually a form of debt, not share capital. In 2024-25, reinvested earnings came to 28 per cent of gross FDI, and inter-corporate loans came to 9 per cent. If we deduct reinvested earnings and inter-corporate loans from gross FDI, the remainder for 2024-25 was only $51 billion (63 per cent of gross FDI). In the same year, foreign investors repatriated/disinvested $51.5 billion (equivalent to 64 per cent of gross FDI). This means that the figure of actual inflows of share capital from foreign investors turned negative even if we disregard outflows on account of Indian investors investing abroad. ︎

- Biswajit Dhar and K.S. Chalapati Rao, Understanding Foreign Direct Investment, 2020, p. 170. Their data are up to the year 2018. ︎

- R. Nagaraj, “Reversing India’s Industrial Decline: Need for Redesigning Policies”, Economic and Political Weekly (EPW), March 15, 2025. ︎

- Dhar and Rao, op. cit., p. 168. ︎

- The list of FDI investment sources includes 13 island countries from the Bahamas to Vanuatu. Dhar and Rao, p. 129. ︎

- R. Nagaraj, “Why has net FDI inflow plummeted?”, The Hindu, June 11, 2025 https://www.thehindu.com/data/net-fdi-inflow-plummeted-india/article69677796.ece ︎

- T.T. Rammohan, “Foreign Banks: A Small Shift That Does Not Change the Basic Policy”, EPW, February 14, 2026. ︎

- Y.V. Reddy, “The Experience of Trying to Reform India’s Banking Sector”, The Wire, August 11, 2017, https://thewire.in/banking/yv-reddy-rbi-banking-reform ︎

- Sanchita Dhingra and Abha Shukla, “Growing Private Equity Investment in India’s NBFC Sector: Analysing Risks”, EPW, May 6, 2023. ︎

- Subrata Panda, “RBI reviewing bank ownership structure, says Governor Sanjay Malhotra”, Business Standard, June 6, 2025. ︎

[Courtesy: Research Unit for Political Economy (RUPE), a Mumbai based trust that analyses economic issues for the common people in simple language.]