❈ ❈ ❈

Liberation Day

Michael Roberts

It’s not April Fools day (1 April). But it might as well be as later today U.S. President Donald Trump announces another barrage of tariffs on imports into the U.S. in what Trump calls ‘Liberation Day’ and what America’s voice of big business and finance, the Wall Street journal, has called “the dumbest trade war in history.”

In this round, Trump is raising tariffs on imports from countries that have higher tariff rates on U.S. exports, ie so-called ‘reciprocal tariffs’. These are supposed to counter what he views as unfair taxes, subsidies and regulations by other countries on U.S. exports. In parallel, the White House is looking at a whole host of levies on certain sectors and the tariffs of 25 per cent on all imports from Canada and Mexico which were earlier postponed are being now reapplied.

U.S. officials have repeatedly singled out the EU’s value added tax as an example of an unfair trade practice. Digital services taxes are also under attack from Trump officials who say they discriminate against U.S. companies. By the way, VAT is not an unfair tariff as it does not apply to international trade and is solely a domestic tax—the U.S. is one of the few countries that does not operate a federal VAT; relying instead on varying federal and state sales taxes.

Trump claims that his latest measures are going ‘liberate’ American industry by raising the cost of importing foreign goods for American companies and households and so reduce demand and the huge trade deficit that the U.S. currently runs with the rest of the world. He wants to reduce that deficit and force foreign companies to invest and operate within the U.S. rather than export to it.

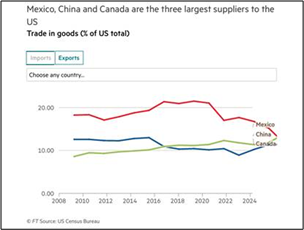

Will this work? No, for several reasons. First, there will be retaliation by other trading nations. The EU has said it would counter U.S. steel and aluminium tariffs with its own duties affecting up to $28bn of assorted American goods. China has also put tariffs on $22bn of U.S. agricultural exports, targeting Trump’s rural base with new duties of 10 per cent on soyabeans, pork, beef and seafood. Canada has already applied tariffs to about $21bn of U.S. goods ranging from alcohol to peanut butter and around $21bn on U.S. steel and aluminium products among other items.

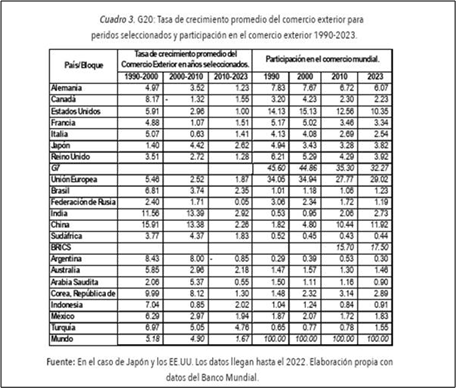

Second, U.S. imports and exports are no longer the decisive force in world trade. U.S. trade as a share of world trade is not small, currently at 10.35%. But that is down from over 14% in 1990. In contrast, the EU share of world trade is 29% (down from 34% in 1990) while the so-called BRICS now have a 17.5% share, led by China at nearly 12%, up from just 1.8% in 1990.

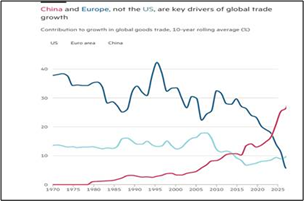

That means non-US trade by other nations could compensate for any reduction in exports to the U.S. In the 21st century, U.S. trade no longer makes the biggest contribution to trade growth—China has taken a decisive lead.

Simon Evenett, professor at the IMD Business School, calculates that, even if the U.S. cut off all goods imports, 70 of its trading partners would fully make up their lost sales to the U.S. within one year, and 115 would do so within five years, assuming they maintained their current export growth rates to other markets. According to the NYU Stern School of Business, full implementation of these tariffs and retaliation by other countries against the U.S. could cut global goods trade volumes by up to 10 per cent versus baseline growth in the long run. But even that downside scenario still implies about 5 per cent more global goods trade in 2029 than in 2024.

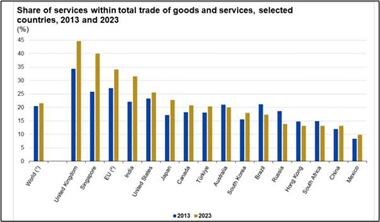

One factor that is driving some continued growth in world trade is the rise of trade in services. Global trade hit a record $33 trillion in 2024, expanding 3.7% ($1.2 trillion), according to the latest Global Trade Update by UN Trade and Development (UNCTAD). Services drove growth, rising 9% for the year and adding $700 billion — nearly 60% of the total growth. Trade in goods grew 2%, contributing $500 billion. None of Trump’s measures apply to services. Indeed, the U.S. recorded the largest trade surplus for trade in services among the trading—some €257.5 billion in 2023–while the UK had the 2nd largest surplus (€176.0 billion), followed by the EU (€163.9 billion) and India (€147.2 billion).

However, the caveat is that services trade still constitutes only 20% of total world trade. Moreover, world trade growth has fallen away since the end of the Great Recession, well before Trump’s tariff measures introduced in his first term in 2016, furthered under Biden from 2020, and now Trump again with Liberation Day. Globalisation is over and with it the possibility of overcoming domestic economic crises through exports and capital flows abroad.

And here is the crux of the reason for the likely failure of Trump’s tariff measures in restoring the U.S. economy and ‘making America great again’: it does nothing to solve the underlying stagnation of the U.S. domestic economy—on the contrary, it makes that worse.

Trump’s case for tariffs is that cheap foreign imports have caused U.S. deindustrialization. For this reason, some Keynesian economists like Michael Pettis have supported Trump’s measures. Pettis writes that America’s “long-term massive deficits tell the story of a country that has failed to protect its own interests.” Foreign lending to the U.S. “force[s] adjustments in the U.S. economy that result in lower U.S. savings, mainly through some combination of higher unemployment, higher household debt, investment bubbles and a higher fiscal deficit,” while hollowing out the manufacturing sector.

But Pettis has this back to front. The reason that the U.S. has been running huge trade deficits is because U.S. industry cannot compete against other major traders, particularly China. U.S. manufacturing hasn’t seen any significant productivity growth in 17 years. That has made it increasingly impossible for the U.S. to compete in key areas. China’s manufacturing sector is now the dominant force in world production and trade. Its production exceeds that of the nine next largest manufacturers combined. The U.S. imports Chinese goods because they are cheaper and increasingly good quality.

Maurice Obstfeld (Peterson Institute for International Economics) has refuted Pettis’ view that the U.S. has been ‘forced’ to import more because mercantilist foreign practices. That’s the first myth propagated by Trump and Pettis.

The second is that the dollar’s status as the premier international reserve currency obliges the United States to run trade deficits to supply foreign official holders with dollars. The third is that U.S. deficits are caused entirely by foreign financial inflows, which reflect a more general demand for U.S. assets that America has no choice but to accommodate by consuming more than it produces.

Obstfeld instead argues that it is the domestic situation of the U.S. economy that has led to trade deficits. American consumers, companies and government have bought more than they have sold abroad and paid for it by taking in foreign capital (loans, sales of bonds and inward FDI). This happened not because of ‘excessive saving’ by the likes of China and Germany, but because of the ‘lack of investment’ in productive assets in the U.S. (and other deficit countries like the UK). Obstfeld: “we are mostly seeing an investment collapse. The answer must depend on the rise in U.S. consumption and real estate investment, to a large degree driven by the housing bubble.” Given these underlying reasons for the U.S. trade deficit, “import tariffs will not improve the trade balance nor, consequently, will they necessarily create manufacturing jobs.” Instead, “they will raise prices to consumers and penalize export firms, which are especially dynamic and productive.”

As I have explained before, t he U.S. runs a huge trade deficit in goods with China because it imports so many competitively priced Chinese goods. That was not a problem for U.S. capitalism up to the 2000s, because U.S. capital got a net transfer of surplus value (UE) from China even though U.S. ran a trade deficit. However, as China’s ‘technology deficit’ with the U.S. began to narrow in the 21st century, these gains began to disappear. Here lies the geo-economic reason for the launching of the trade and technology war against China.

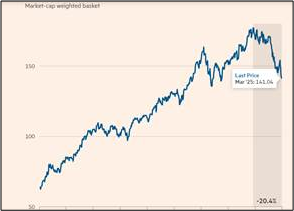

Trump’s tariffs will not be a liberation but instead only add to the likelihood of a new rise in domestic inflation and a descent into recession. Even before the announcement of the new tariffs, there were significant signs that the U.S. economy was slowing at some pace. Already, financial investors are taking stock of Trump’s ‘dumbest trade war in history’ by selling shares. America’s former ‘Magnificent Seven’ stocks are already in in a bear market, ie falling in value by over 20% since Xmas.

The economic forecasters are lowering their estimates for U.S. economic growth this year. Goldman Sachs has raised the probability of a recession this year to 35% from 20% and now expects U.S. real GDP growth to reach only 1% this year. The Atlanta Fed GDP Now economic forecast for the first quarter of this year (just ended) is for a contraction of 1.4% annualised (ie -0.35% qoq). And Trump’s tariffs are still to come.

Tariffs have never been an effective economic policy tool that can boost a domestic economy. In the 1930s, the attempt of the U.S. to ‘protect’ its industrial base with the Smoot-Hawley tariffs only led to a further contraction in output as part of the Great Depression that enveloped North America, Europe and Japan. The Great Depression of the 1930s was not caused by the protectionist trade war that the U.S. provoked in 1930, but the tariffs then did add force to that global contraction, as it became ‘every country for itself’. Between the years 1929 and 1934, global trade fell by approximately 66% as countries worldwide implemented retaliatory trade measures.

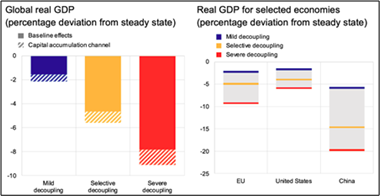

More and more studies argue that a tit-for-tat tariff war will only lead to a reduction in global growth, while pushing up inflation. The latest reckons that with a ‘selective decoupling’ between a (U.S.-centric) West bloc and a (China-centric) East bloc limited to more strategic products, global GDP losses relative to trend growth could hover around 6%. In a more severe scenario affecting all products traded across blocs, losses could climb to 9%. Depending on the scenario, GDP losses could range from 2% to 6% for the U.S. and 2.4% to 9.5% for the EU, while China would face much higher losses.

So no liberation there.

[Michael Roberts worked in the City of London as an economist for over 40 years. He has closely observed the machinations of global capitalism from within the dragon’s den. At the same time, he was a political activist in the labour movement for decades. Since retiring, he has written several books. ‘The Great Recession – a Marxist view’ (2009); ‘The Long Depression’ (2016); ‘Marx 200: a review of Marx’s economics’ (2018): and jointly with Guglielmo Carchedi as editors of ‘World in Crisis’ (2018). He has published numerous papers in various academic economic journals and articles in leftist publications. Courtesy: The Next Recession, Michael Roberts’ blog. ]

❈ ❈ ❈

In Trade War with the US, China Holds a Lot More Cards Than Trump May Think − In Fact, It Might Have a Winning Hand

Linggong Kong

When Donald Trump pulled back on his plan to impose eye-watering tariffs on trading partners across the world, there was one key exception: China.

While the rest of the world would be given a 90-day reprieve on additional duties beyond the new 10% tariffs on all U.S. trade partners, China would feel the squeeze even more. On April 9, 2025, Trump raised the tariff on Chinese goods to 125% – bringing the total U.S. tariff on some Chinese imports to 145%.

The move, in Trump’s telling, was prompted by Beijing’s “lack of respect for global markets.” But the U.S. president may well have been smarting from Beijing’s apparent willingness to confront U.S. tariffs head on.

While many countries opted not to retaliate against Trump’s now-delayed reciprocal tariff hikes, instead favoring negotiation and dialogue, Beijing took a different tack. It responded with swift and firm countermeasures. On April 11, China dismissed Trump’s moves as a “joke” and raised its own tariff against the U.S. to 125%.

The two economies are now locked in an all-out, high-intensity trade standoff. And China is showing no signs of backing down.

And as an expert on U.S.-China relations, I wouldn’t expect China to. Unlike the first U.S.-China trade war during Trump’s initial term, when Beijing eagerly sought to negotiate with the U.S., China now holds far more leverage.

Indeed, Beijing believes it can inflict at least as much damage on the U.S. as vice versa, while at the same time expanding its global position.

A changed calculus for China

There’s no doubt that the consequences of tariffs are severe for China’s export-oriented manufacturers – especially those in the coastal regions producing furniture, clothing, toys and home appliances for American consumers.

But since Trump first launched a tariff increase on China in 2018, a number of underlying economic factors have significantly shifted Beijing’s calculus.

Crucially, the importance of the U.S. market to China’s export-driven economy has declined significantly. In 2018, at the start of the first trade war, U.S.-bound exports accounted for 19.8% of China’s total exports. In 2023, that figure had fallen to 12.8%. The tariffs may further prompt China to accelerate its “domestic demand expansion” strategy, unleashing the spending power of its consumers and strengthening its domestic economy.

And while China entered the 2018 trade war in a phase of strong economic growth, the current situation is quite different. Sluggish real estate markets, capital flight and Western “decoupling” have pushed the Chinese economy into a period of persistent slowdown.

Perhaps counterintuitively, this prolonged downturn may have made the Chinese economy more resilient to shocks. It has pushed businesses and policymakers to come to factor in the existing harsh economic realities, even before the impact of Trump’s tariffs.

Trump’s tariff policy against China may also allow Beijing a useful external scapegoat, allowing it to rally public sentiment and shift blame for the economic slowdown onto U.S. aggression.

China also understands that the U.S. cannot easily replace its dependency on Chinese goods, particularly through its supply chains. While direct U.S. imports from China have decreased, many goods now imported from third countries still rely on Chinese-made components or raw materials.

By 2022, the U.S. relied on China for 532 key product categories – nearly four times the level in 2000 – while China’s reliance on U.S. products was cut by half in the same period.

There’s a related public opinion calculation: Rising tariffs are expected to drive up prices, something that could stir discontent among American consumers, particularly blue-collar voters. Indeed, Beijing believes Trump’s tariffs risk pushing the previously strong U.S. economy toward a recession.

Potent tools for retaliation

Alongside the changed economic environments, China also holds a number of strategic tools for retaliation against the U.S.

It dominates the global rare earth supply chain – critical to military and high-tech industries – supplying roughly 72% of U.S. rare earth imports, by some estimates. On March 4, China placed 15 American entities on its export control list, followed by another 12 on April 9. Many were U.S. defense contractors or high-tech firms reliant on rare earth elements for their products.

China also retains the ability to target key U.S. agricultural export sectors such as poultry and soybeans – industries heavily dependent on Chinese demand and concentrated in Republican-leaning states. China accounts for about half of U.S. soybean exports and nearly 10% of American poultry exports. On March 4, Beijing revoked import approvals for three major U.S. soybean exporters.

And on the tech side, many U.S. companies – such as Apple and Tesla – remain deeply tied to Chinese manufacturing. Tariffs threaten to shrink their profit margins significantly, something Beijing believes can be used as a source of leverage against the Trump administration. Already, Beijing is reportedly planning to strike back through regulatory pressure on U.S. companies operating in China.

Meanwhile, the fact that Elon Musk, a senior Trump insider who has clashed with U.S. trade adviser Peter Navarro against tariffs, has major business interests in China is a particularly strong wedge that Beijing could yet exploit in an attempt to divide the Trump administration. A strategic opening for China?

While Beijing thinks it can weather Trump’s sweeping tariffs on a bilateral basis, it also believes the U.S. broadside against its own trading partners has created a generational strategic opportunity to displace American hegemony.

Close to home, this shift could significantly reshape the geopolitical landscape of East Asia. Already on March 30 – after Trump had first raised tariffs on Beijing – China, Japan and South Korea hosted their first economic dialogue in five years and pledged to advance a trilateral free trade agreement. The move was particularly remarkable given how carefully the U.S. had worked to cultivate its Japanese and South Korean allies during the Biden administration as part of its strategy to counter Chinese regional influence. From Beijing’s perspective, Trump’s actions offer an opportunity to directly erode U.S. sway in the Indo-Pacific.

Similarly, Trump’s steep tariffs on Southeast Asian countries, which were also a major strategic regional priority during the Biden administration, may push those nations closer to China. Chinese state media announced on April 11 that President Xi Jinping will pay state visits to Vietnam, Malaysia and Cambodia from April 14-18, aiming to deepen “all-round cooperation” with neighboring countries. Notably, all three Southeast Asian nations were targeted with now-paused reciprocal tariffs by the Trump administration – 49% on Cambodian goods, 46% on Vietnamese exports and 24% on products from Malaysia.

Farther away from China lies an even more promising strategic opportunity. Trump’s tariff strategy has already prompted China and officials from the European Union to contemplate strengthening their own previously strained trade ties, something that could weaken the transatlantic alliance that had sought to decouple from China.

On April 8, the president of the European Commission held a call with China’s premier, during which both sides jointly condemned U.S. trade protectionism and advocated for free and open trade. Coincidentally, on April 9, the day China raised tariffs on U.S. goods to 84%, the EU also announced its first wave of retaliatory measures – imposing a 25% tariff on selected U.S. imports worth over €20 billion – but delayed implementation following Trump’s 90-day pause.

Now, EU and Chinese officials are holding talks over existing trade barriers and considering a full-fledged summit in China in July.

Finally, China sees in Trump’s tariff policy a potential weakening of the international standing of the U.S. dollar. Widespread tariffs imposed on multiple countries have shaken investor confidence in the U.S. economy, contributing to a decline in the dollar’s value.

Traditionally, the dollar and U.S. Treasury bonds have been viewed as haven assets, but recent market turmoil has cast doubt on that status. At the same time, steep tariffs have raised concerns about the health of the U.S. economy and the sustainability of its debt, undermining trust in both the dollar and U.S. Treasurys.

While Trump’s tariffs will inevitably hurt parts of the Chinese economy, Beijing appears to have far more cards to play this time around. It has the tools to inflict meaningful damage on U.S. interests – and perhaps more importantly, Trump’s all-out tariff war is providing China with a rare and unprecedented strategic opportunity.The Conversation

(The author is a Ph.D. Candidate in Political Science, Auburn University. Courtesy: The Conversation, an Australia-based nonprofit, independent global news organization dedicated to unlocking the knowledge of experts for the public good.)