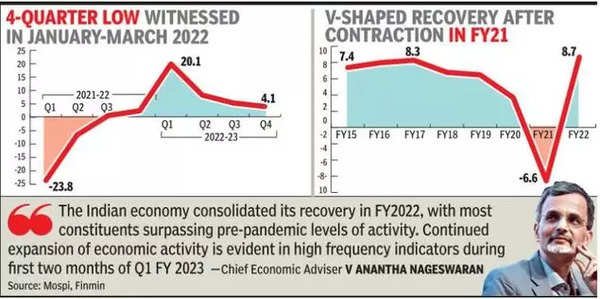

The estimates of India’s Gross Domestic Product for the fourth quarter of 2023 were released on May 31. These show a growth rate of 6.1 per cent over the fourth quarter of the previous year, which is higher than the 4.4 per cent growth that the October-December quarter had recorded over the corresponding quarter of the previous year. Taking the year 2022-23 as a whole, the growth rate of GDP over the previous year comes to 7.2 per cent, higher than the 6.8 per cent expected earlier by both the IMF and the Reserve Bank of India.

The fact that the GDP figure has turned out to be a shade higher than expected earlier, makes not an iota of difference to one’s assessment of the current state of India’s economy. It still means that between 2019-20 and 2022-23, even ignoring the lockdown-induced sharp drop in GDP that occurred in 2020-21, the compound annual point-to-point growth rate of GDP comes to a meagre 2.85 (it was 2.7 per cent on the basis of the earlier fourth quarter expected growth rate); and it is still the case, according to almost every observer, that the 2022-23 growth rate cannot be sustained in 2023-24 because of a slowing down of the growth of various components of aggregate demand. The fact that the Indian economy is being afflicted by stagnation is thus quite indubitable.

The government however, true to its character, has unleashed a propaganda barrage on the basis of the latest GDP figures. Its claim is that India is now the fastest growing economy among the major economies of the world; and that this fact testifies to its deft handling of the economy. What it omits to mention is that among the major economies of the world India had the sharpest drop in GDP during the year 2020-21 that witnessed the pandemic-induced lockdown; its lock-down had been the most draconian of all. The climb back to even the pre-pandemic level of GDP therefore entails an extraordinarily high growth-rate from the low base to which it had sunk. The fact, as mentioned earlier, that if we completely ignore the pandemic year and the one of recovery that immediately follows, and simply compare the pre-pandemic year 2019-20 with a normal post-pandemic year 2022-23, we find an annual growth rate of merely 2.85 per cent, is indicative of a state of stagnation rather than of growth, let alone of impressive growth.

The latest GDP figures however highlight even more markedly a disturbing phenomenon that has been noted by many. The GDP in real terms in 2022-23 is 13.37 per cent larger than in 2018-19; but the unemployment rate according to the data made available by the Centre for Monitoring the Indian Economy (CMIE) was 6.3 per cent in 2018-19, and climbed up to 7.9 per cent in March 2023. Why should the unemployment rate climb up in a period when the GDP is increasing, by no means impressively as we have just seen, but certainly at a rate higher than the rate of growth of population to which the rate of growth of the work-force is linked? In fact the labour force participation rate, that is, the ratio of the labour force to working-age population, has not increased during this very short period. So, why should the unemployment rate increase so sharply?

Indeed the fact that the rise in unemployment rate is not because of any sudden increase in labour supply, but rather because of a fall in labour demand, is confirmed by another piece of evidence from the CMIE. This shows an absolute decline in the number of persons employed, from 408.9 million in 2019-20 to 407.6 million in March 2023. This absolute decline suggests three things: first, the recovery from the economic trough reached in 2020-21 has been more pronounced in less employment-intensive activities and less pronounced in the more employment-intensive activities, such as the unorganised sector that continues to languish because of the blows it received during the lock-down, not to mention the earlier blows in the form of demonetisation and the GST. Secondly, there is a continuous increase in labour productivity that is occurring in the economy, with digitisation increasingly replacing human activity; since the rate of growth of employment is simply the excess of the rate of growth of output over the rate of growth of labour productivity, this fact ipso facto lowers the rate of growth of employment. Thirdly, there have been actual lay-offs in a number of spheres in response to reduced demand for labour, or as a means of enforcing austerity; this would explain the sudden declines we find in the number of employed persons, for instance from 409.9 million in February 2023 to 407.6 million in March.

Some of these very factors however which explain the rise in the unemployment rate also suggest why the GDP growth for Q4 of 2022-23, and hence for 2022-23 as a whole, is itself overestimated. With the new method of estimating GDP, the preliminary estimate, of the sort we now have for Q4 of 2022-23, is arrived at by assuming that the observed growth-rate of organised sector activities, holds also for the non-agricultural unorganised sector. In other words, since data for the unorganised sector take time to come in, the preliminary estimate is made when very little data are available for this sector; because of this the organised sector data are assumed to hold for both sectors taken together. But since the unorganised sector has been badly hit, especially during the pandemic, from which it has not recovered, this method of attributing the organised sector’s growth to both sectors taken together, has the effect of exaggerating the overall growth rate of the economy.

Even within the organised sector, it is the data on the financial performance of listed companies within the private corporate sector, which are available on a quarterly basis, that have an overwhelming weight in the measurement of the growth rate of the sector as a whole; and this gives an additional upward bias to the GDP growth rate figure. This growth figure will no doubt be adjusted downwards later if the CSO is given a free hand and if it is conscientious, but for the time being the exaggerated figure of growth serves the Modi government’s propaganda needs well.

But even as the figures stand, what is absolutely striking is that the growth rate of the manufacturing sector (gross value added) for the year as a whole over the previous one, comes to an abysmal 1.3 per cent. It is the agricultural sector (4 per cent) whose output is subject to wide fluctuations, and the service sector within which “trade, hotels, transport, communications and services related to broadcasting” (14 per cent) have grown the fastest, that have driven up the overall growth rate.

This is significant. The service sector generally thrives on the basis of surplus value generated within the material commodity producing sectors, which is why Adam Smith had categorised workers engaged in the service sector as “unproductive workers”, and also why in the Soviet Union and other East European socialist countries, service sector output was not included in GDP estimation. In addition, service sector growth often reflects the mere commoditisation of a range of activities earlier carried out within the household, and hence does not reflect any genuine addition to the level of activity. Besides, estimating service sector output is fraught with difficulties, especially in the unorganised segment of it. For all these reasons, a high growth-rate of the service sector, especially when it is accompanied by a stagnation of manufacturing, is not necessarily a thing to celebrate.

Besides, the argument that the extrapolation of organised sector’s growth to the unorganised sector exaggerates the actual growth rate, applies with particular force to the service sector. The working people generally spend their incomes, apart from food, on manufactured goods and on the output of the unorganised service sector. The fact that manufacturing output has been virtually stagnant, while unorganised service sector output is unlikely to have done any better, suggests that the consumption of the working people has remained extremely subdued. Added to this is the fact that the growth in government expenditure has been literally stagnant in real terms. Gross fixed capital formation has gone up no doubt, but such growth in investment can scarcely be sustained if consumption and net exports are lagging behind.

The consumption of the working people being subdued is the most disquieting feature revealed by the GDP statistics, which no amount of crowing about India being “the fastest growing economy” in the world, can possibly hide.

(Prabhat Patnaik is Professor Emeritus at the Centre for Economic Studies and Planning, Jawaharlal Nehru University, New Delhi. Courtesy: The author’s blog at networkideas.org.)