From time to time, the Indian authorities acknowledge, albeit softly, that the real incomes (i.e., the incomes after discounting for inflation) of the majority of Indians have been falling.

(1) Data from the Annual Survey of Industries show that gross emoluments per person engaged in the organised factory sector in 2022-23 (the latest available year) were 3 per cent lower than four years earlier, in 2018-19.[1]

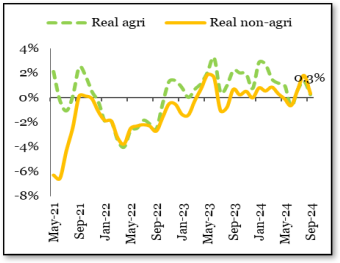

(2) Real rural wages, agricultural and non-agricultural, have remained stuck at virtually the same level for nearly a decade now. The Economic Survey 2024-25 provides the following chart of the picture since May 2021:

Year-on-year Real Growth in Rural Wages, Men

Source: Economic Survey 2024-25

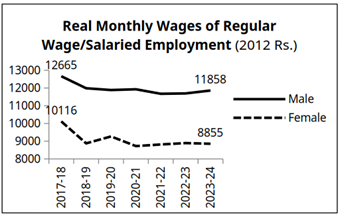

(3) In the period since 2017-18, the real wages of salaried/regular workers have fallen by 6 per cent for men, and 13 per cent for women. Wages are expressed in 2012 rupee terms in the Chart below.

Source: Economic Survey 2024-25

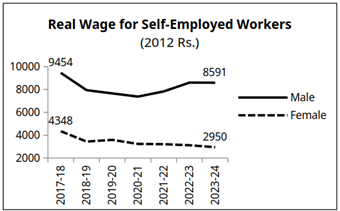

(4) The incomes of self-employed workers have fallen even more steeply over the same period, by 9 per cent for men and 32 per cent for women. (It should further be noted that earnings for self-employed workers are calculated by excluding those self-employed persons who reported earning as zero.)

Source: Economic Survey 2024-25

This reflects the condition of the majority of workers in India. The proportion of self-employed workers was already 52 per cent of the workforce in 2017-18. It has now risen to over 58 per cent in 2023-24. The Economic Survey tries to spin this, saying that “This shift reflects growing entrepreneurial activity and a preference for flexible work arrangements,” but in fact the rising figures of self-employment reflect the desperation of the unemployed to eke out a living somehow, either on the farm, or in petty production or petty trade. Meanwhile the share of workers in regular/salaried jobs decreased from 23 per cent to 22 per cent during the same period.

(5) The real daily wages of casual workers rose by 19 per cent for men and 24 per cent for women between 2018-19 and 2023-24. But then casual workers seem to be getting progressively fewer days of work over this entire period. As a result their total income may not have risen much. For lack of work, the share of casual workers in the workforce declined sharply, from 25 per cent to 20 per cent.

(6) The fall in real incomes appears to be even steeper in some of the newer sectors. Data from an NCAER study of food delivery platform workers show that their real incomes fell by 24 per cent between 2019 and 2022.[2]

Even more surprising are the facts reported in a recent note by a website, ‘Careers360’: The entry-level salaries in two of India’s leading software firms, TCS and Infosys, have stagnated in nominal terms for the past 15-18 years, amounting to a steep fall in real terms: while an Assistant Systems Engineer Trainee at TCS received Rs 3.15 lakh per annum in 2007, he/she received Rs 2.95-3.36 lakh per annum in 2024, a 60 per cent fall in real terms. A Systems Engineer Trainee at Infosys Rs 3.25 lakh per annum in 2010, and Rs 3.6 lakh per annum in 2024, a 49 per cent fall in real terms. Careers360 says that the situation is similar in all the other top software firms.[3] The note points out that this has taken place even as the costs which these engineers would have had to incur for their education have multiplied; this implies that they will take much longer to repay their educational loans.

Demand depression

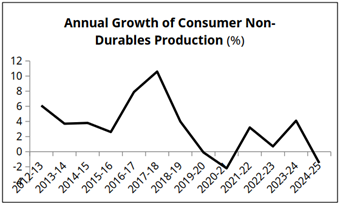

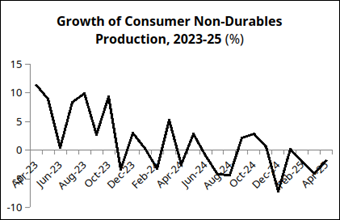

All these developments have resulted in the depression of demand for ordinary goods of mass consumption. This can be seen in the Index of Industrial Production (IIP) data. The growth of consumer non-durables – largely items of daily use such as soap, detergent, toothpaste, tea powder, food products, medicines, paper, and so on, has been trending downward for some years.

Source: Index of Industrial Production

Well before the Covid lockdown, non-durables production was already slowing down. During the Covid period, expectedly, production fell outright; it then recovered after the lockdown ended. However, in the recent period, production appears to be falling outright again. The chiefs of major fast-moving consumer goods (FMCG) firms have been widely quoted in the media bemoaning the lack of demand.

Source: Index of Industrial Production

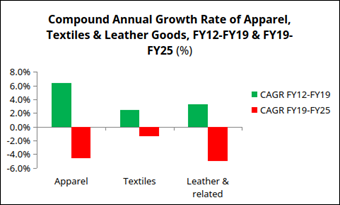

Some other items of mass consumption are strangely classified by the IIP as “consumer durables”, presumably on the ground that they last more than a year. However, it makes more sense to group textiles, apparel, and leather goods with soap and toothpaste rather than with automobiles and electronic items. The production of textiles, apparel and leather goods provides a similarly grim picture.

Source: Calculated from Index of Industrial Production

The above data provide glimpses into the depression of consumption by the vast masses of Indians, not only in relative terms, but in absolute terms.

Since the industries manufacturing goods of mass consumption tend to be relatively labour-intensive, the paucity of demand for these goods would have an impact on employment itself. For example, it is estimated that the entire textile value chain, from fibre to spinning to fabric to processing to garments, generates employment for 45 million – one of the largest sources of employment in the country. Government efforts to generate demand for Indian textiles are focussed exclusively on increasing India’s exports (see, for example, the discussion in the Economic Survey 2024-25), which accounts for about a fifth of demand. The growth of domestic demand for textiles is linked to a rise in people’s incomes. India’s fibre consumption per capita is 5.5 kg, which is less than half the world average; by comparison, the average for South Asia is 7.1 kg, Latin America 8.9 kg, and China 14 kg. A similar story could be told of other items of mass consumption.

This paucity of demand is not a temporary phenomenon, occasioned by demonetisation, lockdowns, or the like. It is an underlying condition of the Indian economy as a whole. Rather, India’s spell of rapid growth during 2004-12 appears to have been a temporary phenomenon, triggered by flows of footloose international capital. Since 2012, growth has slowed, demand has stagnated, the private corporate sector has refused to embark on a new investment boom, and incomes in the vast informal/unorganised sector have shrunk. Episodes in the last decade such as demonetisation, the imposition of the Goods and Services Tax regime, and the Covid lockdown no doubt worsened conditions, but even after some years have passed, the stagnation of demand has continued. The plethora of Government hand-out schemes are mere palliatives to divert people from realising the need for fundamental change.

(All figures in this article are rounded off.)

Notes

- Deflated by CPI (Industrial Workers).

- RUPE, “Who Loses, Who Gains?”, October 7, 2023, https://rupeindia.wordpress.com/2023/10/07/who-loses-who-gains/#more-2524

- Careers360, “The Harsh Truth Behind College Placements with TCS, Infosys, Wipro, Accenture, Cognizant etc…”, June 5, 2025. https://engineering.careers360.com/articles/the-harsh-truth-behind-college-placements-tcs-infosys-wipro-accenture-cognizant-etc

[Courtesy: Research Unit for Political Economy (RUPE) is a Mumbai based trust that analyses economic issues for the common people in simple language.]