It’s a paradox that has periodically recurred in recent times. Financial indicators are hugely favourable from the point of view of those who benefit from them, even when the performance of the real economy is poor or dismal. In this Covid-afflicted year, that paradox has manifested itself with greater intensity. And with a difference. Even while the real economy remains in contractionary mode, not only have stock market returns exploded, but India’s stock of foreign exchange reserves, considered a measure of the country’s economic health from Independence to the balance of payments of crisis of 1991, have registered record-breaking increases.

While stock markets are no indicators of economic health, news that the BSE Sensex breached the 48,000 mark on January 4 had to be acknowledged as significant. The figure not only reflected a huge 85 per cent rise relative to the low the Sensex touched in March 2020, when the devastating economic consequences of Covid pandemic had begun to be felt, but is also significantly higher than the pre-pandemic peak of a little over 41,500. More importantly, India’s central bank has been accumulating foreign exchange reserves at an astounding pace. India’s foreign reserves rose by $105 billion between 27 March and 25 December 2020, to touch $580 billion. That increase was more than double the increment of $46 billion recorded in a comparable period of the previous year (29 March to 27 December 2019).

Normally, a strengthening foreign reserve position is potentially a better indicator of economic health than stock market buoyancy. But judgement on that account must be based on an assessment of the factors that drive the remarkable accumulation of reserves. The breakdown of elements contributing to the increment in the dollar value of reserves over the period April to September 2020 was only recently released by the RBI. Of the $66.9 billion rise during this period, 15.5 billion was on account of valuation changes, influenced by the composition including the currency composition of available reserves. So, the material increment in reserves over April to September attributable to balance of payments developments was $51.4 billion. But even that was dizzyingly high when compared with just $19.1 billion over the corresponding period of the previous year.

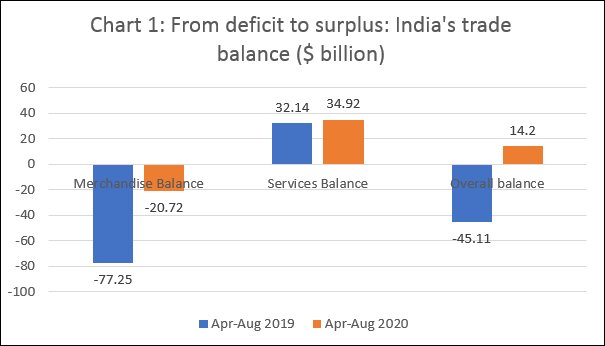

What is striking is that of this $51.4 billion increase as much as $34.7 billion was contributed by a current account surplus, or an excess of receipts other than capital flows (from exports and remittances, for example) over expenditures of foreign exchange (or outflows such as payments against imports, interest on foreign debt or dividends to foreign investors). Only $16.7 billion of the increment in reserves during this period was due to net inflows of foreign capital. This is a reversal of earlier trends when, India’s current account tended to be consistently negative and inflows of foreign capital in excess of that needed to cover that deficit contributed to an increase in reserves. Thus, over the April-September of the previous year 2019, India’s balance of payments showed a current account deficit of $22.6 billion, and it was only because net capital inflows were a much larger $41.7 billion, that the country recorded a $19.1 billion increase in reserves (exclusive of valuation changes). To summarise, the record reserve accumulation seen hitherto in Covid-hit financial year 2020-21 was substantially the result of the rather unusual development that India’s expenditure of foreign exchange for its current transactions fell short of its current account receipts, principally in the form of export earnings and remittances. Foreign capital inflows played a role but made a much smaller contribution.

The shift from a deficit to a surplus on the current account is surprising also because it occurs in a year when the global downturn impacted India’s merchandise export earnings adversely and resulted in job losses among immigrant workers abroad who are the source of India’s large remittance receipts. Lower foreign receipts from export earnings and remittances should have widened India’s ‘normal’ current account deficit, rather than transformed it into a surplus. Consider the figures. India’s export of goods over April to September fell from $159 billion in 2019 to $125 billion in 2020. There was only one month of those six (September), when the export figure was marginally higher in 2020 when compared with 2019. But even that positive ray of hope has vanished with exports falling again in the subsequent three months. Over April to December India’s export earnings fell from $238 billion in 2019 to $201 billion or by close to 16 per cent. Though net exports of services remained strong, it was at $41.7 billion in April-September 2020 almost the same as in the corresponding months of the previous year. There was an aggregate loss on account of falling revenues from exports.

This loss is unlikely to have been made up by increased remittances. It is true that repatriation of past savings by returning migrants who lost their jobs would have, in the short run, neutralised the fall in regular remittances resulting from those job losses. But if the April to September period, for which figures are available, is any indication, remittance receipts have in fact fallen. The inflow on account of “secondary income” consisting in India’s case largely of workers’ remittances fell from $38 billion during April to September 2019 to $35.4 billion during April to September 2020.

If despite these adverse trends the current account balance in India’s external payments has turned significantly positive from being negative, it is only because of a sharp fall in the country’s import bill. From $248 billion over April to September 2019, India’s import bill fell to $150 during the same months of 2020. The corresponding figures for April-December are $364 billion and $258 billion respectively, which amounts to a decline of 29 per cent. The demand for imports and expenditures on them fell because of the economic contraction resulting from supply shocks and demand recession.

Both oil and non-oil imports contributed to the decline in imports. Oil imports fell from $211 billion during April to October 2019 to $145 billion during the corresponding months of 2020. The figures for non-oil imports during those months registered a decline from $75 billion to $38 billion. While oil price volatility played a role in keeping oil import values down, much of the decline in oil prices had occurred even by 2019. Thus, in the case of both oil and non-oil imports, it was the Covid-19 and subsequent harsh-lockdown induced collapse of the economy that reduced the demand for imports. In the event, despite a fall in export revenues the current account shows a large positive value in the Covid year. To the extent that the remarkable increase in India’s foreign exchange reserves in recent months was driven by the current account surplus, it is a fall-out of the crisis affecting the economy rather than an indicator of improving economic health. The accelerated accumulation of foreign reserves in 2020 was substantially the result of the collapse in imports induced by the recession that gripped the Indian economy both because of the pandemic and the government responses to it in the form of a harsh lockdown and a measly stimulus package.

But that is not all. Reserves rose also because of the net inflow of foreign capital in a period when there was no longer any deficit on the current account that had to be financed. The April to December months have seen large inflows of foreign direct and portfolio investments and some external commercial loans contracted at low interest rates. With no net current outflows to finance, these sums too, after adjusting for capital outflows, contributed to the rapid rise in India’s foreign exchange reserves. Over April to September 2020 those flows contributed a third of the increment in reserves.

A corollary of the large inflows of foreign capital, especially portfolio and FDI flows, was that a stock market that had turned bearish and collapsed in March 2020, when the pandemic struck, soon turned around and has since experienced a boom even when the effects of the pandemic have devastated the real economy. Given real economy trends, it is difficult to believe that the exuberance that investors in India’s equity markets display is rational and justified by expectations of an impending V-shaped recovery that would take earnings to levels that warrant today’s stock prices. Two factors seem to have played a role in fuelling irrational exuberance. The first is the availability of large volumes of zero-cost liquidity in international financial centres, which trigger a rush of speculative capital to markets worldwide. The second is the belief that a business-friendly government in India, which brooks no opposition to pro-business ‘reforms’, will ensure that markets do not collapse from their unjustifiable highs.

The result has been that record-setting numbers have been registered on the financial and monetary fronts in a context where the India economy is barely creeping out of severe recession. Despite the marginal revival of economic activity following the withdrawal of lockdown measures, there is much uncertainty with regard to a return to reasonable growth. Even optimistic official projections of GDP growth expect a contraction of more than 7 per cent in GDP over 2020-21. However, since the mild buoyancy triggered by purchases during the festive season is unlikely to persist, the actual contraction could turn out to be sharper.

Under normal circumstances the persisting recession should have given punters in equity markets a reason to pause. But the reality is that it is the crisis that feeds speculation, with central banks releasing ever growing sums of cheap liquidity into the system, and governments like those in India striving to ensure, as long as they can, that speculators are not disappointed. The result is that paper “wealth” at the peak of the pyramid explodes, inequality increases, but the crisis remains unaddressed in the hope that the vaccine will do the needful.

(C.P. Chandrasekhar is currently Professor at the Centre for Economic Studies and Planning, Jawaharlal Nehru University, New Delhi.)