[India’s large capitalists and India’s people are both facing problems at present. These problems appear to be direct opposites of each other; but in fact they are two faces of the same phenomenon.

In the first part of this article, we described the financial situation of the corporate sector. In the second part, we described the financial situation of the people. In this third part, we link the two.]

III. Accumulation amid Distress

In the previous two parts we saw that the corporate sector and the banks are sitting on a mountain of cash; on the other hand, large numbers of working people are facing distress, and are resorting to borrowing to meet their basic needs.

To place the present situation in context, let us recall the state of affairs five years ago, during the Covid lockdown. At the time, the lockdown had wiped out the livelihoods and savings of vast masses of people; millions of workers had left the cities to take refuge in their villages; many were borrowing to meet their bare consumption needs; the education of millions of children was disrupted; many were struggling to get medical care.

In that same period, however, India’s share markets soared. Private corporate investment was said to be on the cusp of a new boom. By December 2020, the Sensex had risen 70 per cent from its April low. Financial analysts were euphoric. What explained this disconnect between the state of the people and the state of the share market?

The neoliberal view of investment

Neelkanth Mishra, at the time chief India strategist for Credit Suisse and a prominent commentator in the business press, explained this heady optimism in a December 2020 interview with Bloomberg Quint.[1] The interview is instructive as a candid presentation of the neoliberal view of private investment. (Mishra has since been appointed to the Prime Minister’s Economic Advisory Council.)

Mishra estimated that the lockdown had cost the Indian economy Rs 20 trillion. He nevertheless claimed that “75 per cent of this loss didn’t have a lasting impact”:

We call it ‘water under the bridge’. What people didn’t earn, they didn’t consume. So the lasting implications were very low.

In his view, it was precisely big firms which drove growth; so the future of the economy was linked to the growth of these firms, at whatever cost to the rest of the economy and its people. The drastic cost-cutting measures adopted by these large Indian firms

pushed the pain of the lockdown to the bottom 30-40 per cent of India’s enterprises and individuals. From an inequality perspective that’s a disastrous outcome but from an economic momentum perspective that’s actually the best possible outcome.

The lockdown thus, in Mishra’s view, turned out to be good for growth: “The top 10-20 per cent of India’s companies, households and individuals, which spend the most, came out of the lockdown with a better balance sheet because their consumption was severely impacted while their income was secure. On the other hand, the bottom 50 per cent saw a deteriorated balance sheet because their income was impacted while they still had to maintain their basic consumption.” The incremental savings of the top 10-20 per cent, he asserted, were likely to drive investment, consumption and hence growth in the coming period. “That is the economic stimulus that has come through”.

The share markets appeared to agree with Mishra’s view, as large inflows of funds sent share prices soaring.[2] Foreign investors were in the lead at the time, with domestic investors following.

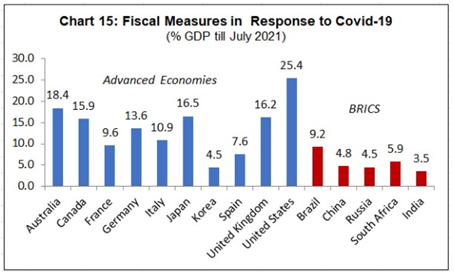

Official policy, too, in the subsequent period reflected this understanding. India’s fiscal response to Covid-19, as a percentage of its GDP, was not only smaller than the response of advanced countries, but also that of other BRICS countries. While the Government distributed grains from its foodstocks free, it held back on other spending. Unlike other countries, which focussed on ‘demand-side’ measures, India focussed on ‘supply-side’ measures, i.e., measures intended to spur private investment. It considered this its unique contribution to the global Covid response.

Source: International Monetary Fund, Database of Fiscal Policy Responses to Covid-19, October 2021. Data pertain to additional spending or foregone revenues.

In the words of the Government’s Economic Survey 2021-22,

[a] distinguishing feature of India’s response has been an emphasis on supply-side reforms rather than a total reliance on demand management. These supply-side reforms include deregulation of numerous sectors, simplification of processes, removal of legacy issues like ‘retrospective tax’, privatisation, production-linked incentives and so on.

The Government claimed that its policy would lead to a “V-shaped recovery”, that is, the steep drop in economic activity as a result of the lockdown would be cancelled out by a steep rise thereafter.

Corporate investment depends on the state of demand

In a sense, the last four years have provided a natural experiment testing this argument. The evidence is overwhelming: It shows that, no matter how much the State gifts large capitalists in the form of cash or assets, capitalists will not undertake investment unless they think doing so will add to their profits. The fall in the incomes of the bottom half of the population, which Mishra celebrated as “the best possible outcome”, has not led to corporate investment. Whether the corporate sector invests in increasing production finally depends on the state of demand in the economy as a whole (aggregate demand).

Why is there a problem of demand in India? India has no shortage of want – rather, it is marked by large-scale want of the basic necessities of life for the mass of working people – but that want is not backed by purchasing power, which is what is needed to translate it into demand in the economy.

India’s underlying paucity of demand is one of the basic features of its economy. This long-term paucity of demand arises from the nature of India’s political economy: its production relations internally and its relationship to a world economy dominated by imperialism. For the underlying state of demand to change, there needs to be a democratic change in production relations and the social order. (This subject demands a more detailed discussion, which we will not attempt here.) In the absence of such change, demand remains stunted and distorted.

On this base of stunted and distorted demand, euphoric surges of growth do take place from time to time, triggered by one or the other abnormal phenomenon, such as – in the late 1980s, large inflows of external commercial borrowings; in the mid-1990s, a brief spike in luxury goods production; in the 2003-08 period, a surge in foreign capital inflows. The last-named episode left a deep impression on India’s business tycoons. They keep harking back to the boom of the first decade of this century as if that were the ‘normal’, and the slump since 2011 were the aberration, but the reverse is the case.

The mirage of export-driven growth

A country’s output can be divided into different types of demand: private consumption demand, Government consumption demand, private investment demand, Government investment demand, and foreign demand, that is, net exports (exports minus imports). Thus

Private consumption + Government consumption + private investment + Government investment + net exports = national income.

The Government has staked much on the growth of exports as the driver of overall growth. In 2014, it announced the ‘Make in India’ programme; this was re-branded in 2020 as Atmanirbhar Bharat in the wake of Covid-19, when the Government hoped to attract multinationals who were said to be leaving China. The Atmanirbhar package included the Production Linked Incentives scheme, whereby selected large industrial producers in specified industries (at present 14 industries) would be provided subsidies on the value of incremental sales. The idea was to promote large Indian firms or conglomerates as ‘national champions’, who commanded the resources to make themselves internationally competitive.

However, this programme has not shown results: India’s goods exports have stagnated for the last decade at between 1.6 and 1.8 per cent of world exports, and that share is reported to have actually declined in 2024. There is also little sign that India’s biggest conglomerates are trying to compete internationally. At any rate, given the current global uncertainty centered on international trade, with India’s largest export destination (the US) putting extraordinary pressure on India, the hope of powering the growth of India’s economy through exports is dim. Even if a trade deal is struck with the US, it is likely that net exports to the US will fall, as the very purpose of the deal is to expand India’s imports from the US. Such a reduction in net exports would shrink demand in India’s economy further.[3]

Attempts to boost corporate profit, at the cost of aggregate demand

Net exports will thus not provide a stimulus to investment, and private consumption, as we have seen is depressed. Nor will the corporate sector, however flush with funds it may be, step up on its own. To state an obvious truth: capitalists do not produce in order to fulfill some material need – either their own or of the people. For them, the purpose of production is to realise profits and thereby accumulate capital. If, by producing commodities, they are unable to accumulate capital, they will stop producing. Equally, if they are able to accumulate capital without producing anything, they will do so. It is only when producing commodities enables them to accumulate capital that they will produce, and only when expanding productive capacity enables them to accumulate more capital that they will carry out productive investment.

If India’s large capitalists feel there is not enough demand to warrant an expansion of output, they tend to seek other methods of accumulation – such as speculation, land acquisition, privatisation, State subsidies (including tax concessions), State-controlled contracts for infrastructure or weaponry, and so on. In all these the role of the State as their handmaiden is crucial. Importantly, given the constraints of India’s existing political economy, these methods boost corporate demand at the cost of the rest of the economy and its people – hence at the cost of aggregate demand. Below we take some instances of this.

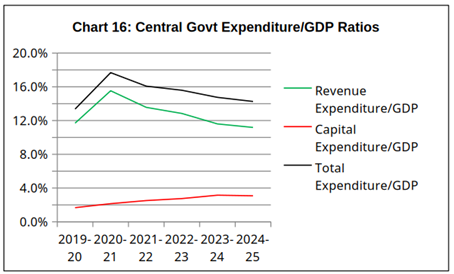

1. Shift in Government expenditure: In order to directly boost demand for the corporate sector, the Central government has increased its capital expenditure (including infrastructural spending, e.g. the building of highways) as a percentage of GDP. Normally, this would be considered a good thing: after all, capital expenditure creates lasting physical assets. The catch is that the Government is not increasing capital expenditure by increasing its total spending. On the contrary, to satisfy the demands of international credit rating agencies such as Standard & Poor and Moody’s, it is actually bringing down its overall spending as a percentage of GDP. (In terms of the equation given earlier, the sum of Government consumption and Government investment is shrinking.)

In order to achieve this reduction in overall spending, the Central government has sharply reduced what is called its ‘revenue expenditure’ as a percentage of GDP. However, it is revenue expenditure (in the form of salaries, welfare expenditures, subsidies, etc) that comes directly into people’s hands. So the reduction of revenue expenditure as a proportion of GDP further dampens overall demand in the economy.

Source: RBI, Handbook of Statistics 2024-25.

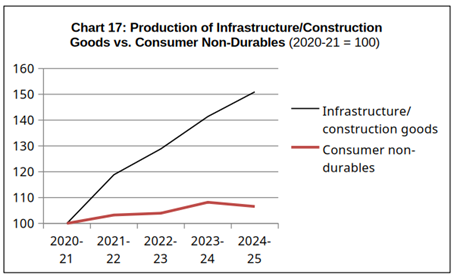

The effect of this pattern of Central government expenditure – viz., more spending for the corporate sector, less spending for the people – is reflected in the respective growth rates of production of infrastructure/construction goods and production of consumer non-durables (i.e., items of ordinary mass consumption such as soap, detergent, toothpaste, tea powder, food products, medicines, paper, and so on), as shown in Chart 17. The items of mass consumption are also more employment-intensive than infrastructure/construction goods, so this pattern of growth has an impact on industrial employment as well.

Source: Index of Industrial Production.

Any Government expenditure creates some demand. However, the major recipient of Government capital spending is the private corporate sector (in the form of infrastructure contracts). When demand is not growing, the private corporate sector may think it wiser to simply pocket the profits of such Government expenditure, not expand production. By contrast, the entire income that comes to the working people gets spent; this in turn leads to further growth of demand (the ‘multiplier effect’). So a shift of Government expenditure from revenue expenditure to corporate sector-oriented capital expenditure can lead to a reduction in overall demand even if total Government expenditure remains the same. This would be even more so if total expenditure actually shrinks as a percentage of GDP.

2. Ousting of other producers: Secondly, even if the market as a whole stagnates or shrinks, the top segment of the corporate sector can maintain the size of its market by ousting its competitors. In this, Government policy measures (demonetisation in 2016, the imposition of the GST system in 2017, and the Covid lockdown in 2020-21) have helped the large corporate sector by eliminating a large number of small firms. A 2022 study estimated that the sales of smaller firms, with capital of less than Rs 5 crore, had shrunk by 14 per cent since the pandemic.[4] There appears to have been some revival of small firms since then, but the losses suffered in that period have left their scars. The workforce in the informal manufacturing sector shrank by almost 5 million between 2015-16 and 2022-23.[5]

There also appears to be increasing concentration within the corporate sector itself. Former RBI Deputy Governor Viral Acharya argues that the increasing concentration within the corporate sector, in particular the growing share of the ‘Big 5’ conglomerates (the Mukesh Ambani Group, the Tata Group, the Aditya Birla Group, the Adani Group, and Bharti Telecom) has allowed top firms to mark up prices more steeply, thereby increasing their profit margins.[6]

3. Corporate capture of health, education, conveyance: In order to boost corporate demand, the Government is systematically promoting corporate capture of certain services, and this directly impinges on the consumption of the people. The Corona package promoted and subsidised private investment in ‘social infrastructure’ (education and healthcare). The effect of such reforms is not to expand education and healthcare, but to commoditise it and hand over a larger share of it to the private corporate sector. Take one example, the public-private partnership (PPP) scheme for hospitals:

Thousands of crores worth of public hospital buildings built over decades of investment to strengthen the public health system and several lakh crores worth of public land are either in the process of being handed over or have already been given to private entities across India. It’s ostensibly happening to upgrade hospitals and build medical colleges through the PPP (public-private partnership) mode.

This process of partnering with the private sector received a push in 2017 when the central government and Niti Aayog, in consultation with the World Bank, recommended operating government hospitals with 300 or fewer beds and setting up medical colleges under the PPP mode. In 2020, the Centre unveiled its viability gap funding scheme, under which it would provide 30%-40% of the capital expenditure for private entities to set up such colleges and the state government would provide another 30%-40%. It further recommended 25% each from Centre and state for the operation and maintenance cost of each project for the first five years. Niti Aayog has been pushing PPPs for running dialysis units, cardiac care and oncology departments and diagnostics, and there has been an explosion of such PPPs across India.[7]

With privatisation, free outpatient consultation and diagnostics get discontinued. While a small proportion of beds are meant to be kept aside as free beds, this is so only on paper. At any rate the bulk are to be paying beds. This leads to a hike in medical costs for individuals: In rural areas, the costs of hospitalisation in private hospitals is six times higher than public hospitals; in urban areas, eight times higher.[8]

These processes have been underway for some time, and effects are visible. During the period of liberalisation, the share of monthly per capita expenditure spent on health has risen. A recent study, citing data of a large household survey, shows that between 2014 and 2017-18, Indian households’ health-related spending rose twice as fast as their overall spending.[9] As a result, health-related spending would have taken a greater share of total spending. And with increasing privatisation, this process is set to intensify.

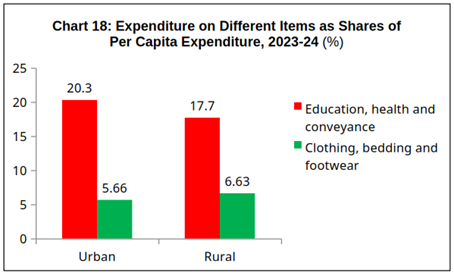

The education sector has been undergoing a similar process of privatisation, and public transport is being silently replaced with private transport (such as two-wheelers). Significantly, the combined expenditures on education, health and conveyance are around three times the expenditures on clothing, bedding and footwear (Chart 18).[10] As expenditure on privatised services has grown, it has pre-empted a larger share of the incomes of working people, leaving less for spending on mass-consumption industrial goods. This has contributed to the visible stagnation in demand for such goods.

Source: National Sample Survey, Household Consumption Expenditure Survey 2023-24.

4. Capture of land and natural assets: The Central government has also taken steps to hand over large swathes of land and associated natural resources to the corporate sector. As part of its Corona package, it liberalised private investment in coal (allowing extraction without specifying end-use) and minerals. It made sweeping changes to environmental laws to allow post-facto clearances (effectively legalising illegality), and to prevent any public questioning of, or opposition to, environmental clearances. More recently, the Central government amended the Forest Conservation Act, 1980 so as to effectively nullify the Forest Rights Act of 2006, and facilitate the corporate grabbing of forest land.[11] It rammed through various projects, such as the Adani acquisition of land in the Hasdeo forest of Chhattisgarh for coal mining. All these measures devastate the subsistence livelihoods of the people of these regions.

The term ‘resource curse’ refers to the observed fact that countries endowed with rich natural resources tend to wind up with lower growth and greater poverty. The theories advanced by economists to explain this observation depict the resource curse as if it were almost a natural or geographical phenomenon, whereas it is actually a social phenomenon. That is, it reflects the colonial or neocolonial domination by industrially developed countries over the resource-rich regions of the world, preventing the people of these regions from exercising control over their own resources. It is this domination, not any natural curse, that keeps the local people in backwardness and poverty. When the extraction ends, the resources are exhausted, the environment is permanently damaged, and there has been no real development of local productive forces – if anything, the reverse.

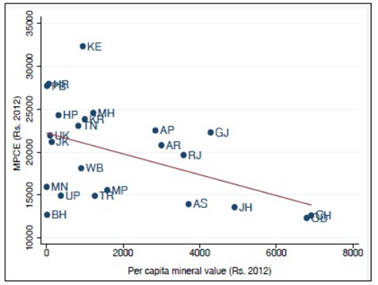

Indeed, the regions richest in mineral resources in India are also the poorest. Chhatisgarh, Odisha and Jharkhand, which have the highest mineral wealth per capita, also have the lowest monthly per capita expenditure (see Chart 19). During the period of liberalisation, the gap between the income levels of the mineral-rich states and other states has widened. Within the mineral-rich states a small elite has benefited: The gap between the incomes of tribals and non-tribals widened in all states, but it widened the most in the mineral-rich states.[12]

As Amit Bhaduri argues, with the capture of land, forest and natural resources by corporate firms, output may rise despite a fall in employment (output per worker in the corporate sector is 12 times that in agriculture); the composition of output itself changes, catering to demand from those with more purchasing power; and the accumulation of wealth is greatly accelerated. Indeed, he remarks, “It opens a far more effective way for corporations to acquire more wealth in a shorter period than profit from production would have made possible.”[13]

Chart 19: Monthly Per Capita Expenditure of Different States

and Mineral Value Per Capita (2012)

Source: Economic Survey 2016-17, vol. I.

At the same time, these processes devastate livelihoods and depress the consumption of the people further.

In conclusion

To conclude: India’s economy has long been marked by an underlying problem of demand. From time to time, there have been euphoric surges of growth, due to one or the other temporary factor. In such periods, large domestic capitalists have been able to rapidly accumulate wealth. But after these surges have petered out, the problem of demand has come to the fore once again.

Another solution to the demand problem is export-oriented growth. Even if we ignore the problems inherent to this model, the results of successive Governments’ efforts to promote exports of manufactured goods have been very poor. And in the present world situation, India’s exports are not going to drive its growth.

In such a situation, large capitalists demand that the State revive the accumulation process by hook or crook, as it were. The Government could increase its spending, a decision which is in its own control, unlike the case of private consumption or private investment. However, in the period of ‘liberalisation’ and globalisation, Government spending has been increasingly constrained by the dictates of international financial capital, which does not approve of increased Government spending.[14] This shuts off one method of relieving the demand problem. And the State’s attempts to boost demand by fueling bank credit growth yield little result, because large capitalists have little need of credit (since they see no profit in expanding production).

So the State turns to predatory measures, predating on the people, in order to help large capitalists’ accumulation process. But by eating into the incomes of the people and undermining or destroying their very livelihoods, the State winds up actually restricting demand even further. In this way, the process is contradictory; leading to another round of shrinking demand.

That is why the corporate sector’s pockets are stuffed with cash, and the banks are groaning with a surfeit of funds, but investment, the engine of growth, has come to a halt.

Notes

- Bloomberg Quint, “Covid-19 Pandemic’s Lasting Cost On Indian Economy Smaller Than Expected: Neelkanth Mishra”, December 18, 2020. https://www.bloombergquint.com/economy-finance/pandemics-lasting-cost-on-indian-economy-smaller-than-expected-neelkanth-mishra ︎

- This does not necessarily mean that share market investors actually believed an economic recovery would take place. It means that they anticipated that the average opinion among investors would expect the average opinion of investors to be that there would be a recovery. (See Keynes on “professional investors” in The General Theory of Employment, Interest and Money, Chapter 12.) ︎

- To explain this: When an Indian firm exports an additional Rs 1 crore worth of goods to another country, that expands India’s market to that extent. But if a foreign firm exports an additional Rs 1 crore of goods to India, that reduces the market for Indian producers to that extent. As a result of the trade deal being negotiated with the US, imports from the US may grab a larger share of India’s market, thus shrinking demand for Indian producers. ︎

- P. Bhandari and A. Chaudhary, HSBC Research, November 2022, cited in Viral Acharya, “India at 75: Replete with Contradictions, Brimming with Opportunities, Saddled with Challenges”, Brookings Papers on Economic Activity, March 2023. ︎

- National Sample Survey, 73rd Round, and Annual Survey of Unorganised Sector Enterprises, 2022-23. ︎

- Viral Acharya, op. cit. ︎

- Rema Nagarajan, “PPP = Transfer of hospitals built with public money into private hands”, Times of India, July 10, 2025. ︎

- Ibid. ︎

- In nominal terms, i.e., without discounting for inflation, per capita spending rose by 53 per cent in the rural areas, and 41 per cent in the urban areas; but per capita spending on health rose 97 per cent in rural areas and 93 per cent in urban areas. Indranil Mukhopadhyay, Montu Bose, and Rahul S. Reddy Kadarpeta, “Contested Claims: Making Sense of the Decline in Out-of-pocket Expenditure”, Economic & Political Weekly, September 6, 2025. The data is of the Consumer Pyramids Household Survey (CPHS) carried out by the Centre for Monitoring the Indian Economy (CMIE). ︎

- National Sample Survey, Household Consumption Expenditure Survey 2023-24. As the survey methodology has changed from 2022-23 on, we are unable to compare expenditures over time. ︎

- Kanchi Kohli and Manju Menon, “Environmental regulation and post-Covid 19 economic recovery”, November 24, 2020, Heinrich Böll Stiftung, https://in.boell.org/en/2020/11/24/environmental-regulation-and-post-covid-19-economic-recovery ︎

- Economic Survey 2016-17, vol. I, p. 293. We do not, however, consider this ‘internal colonialism’, though some have argued this. Internal colonialism suggests that some other regions within India benefit at the expense of the colonised regions, which is not the case. The extraction of natural resources from underdeveloped regions benefits a small class domestically and international capital. ︎

- Amit Bhaduri, “Danger Zones of High Economic Growth”, EPW, October 22, 2016. ︎

- The reasons international investors oppose an increase in Government spending need to be explained separately, but in essence, by suppressing domestic demand in India, international investors are able to capture the maximum gain from their investments here. ︎

[Courtesy: Research Unit for Political Economy (RUPE), a Mumbai based trust that analyses economic issues for the common people in simple language.]